🚨 Get Covered Illinois report: Effectuated enrollment down 12.4%, ~52K have lost coverage as of May

Over 684,000 have lost ACA coverage due to Trump/GOP policies across just 15 states so far

The Illinois Health Benefits Exchange, which operates the states new ACA exchange, Get Covered Illinois, has published their June advisory committee meeting slide deck. Let’s dig in!

Enacted state healthcare legislation

HB 0111: DOI Budget Appropriation: Approval of DOI’s budget appropriation request, which includes $72,345,000 in resources to support GCI’s operation and additional headcount to support the hiring of six new GCI positions.

SB 3815: Health Insurance Enrollment Protections: Prohibits insurers from denying enrollment in coverage when an individual has past-due premiums from a previous plan unless specific conditions are met. Prohibiting insurers from stacking past-due premiums on the initial binder payment and requires insurers to offer a 12-month payment plan for past-due premiums.

SB 3508: Annual DOI Administrative Cleanup Bill: Among other insurance-related items, allows GCI to adopt new federal regulations more easily to ensure timely compliance with ACA provisions.

Notice of Benefit and Payment Parameters

The Notice of Benefit and Payment Parameters (NBPP) is the annual rule issued by the Centers for Medicare & Medicaid Services (CMS) that contains new and updated regulations for ACA marketplaces. The final rule for the 2027 plan year was issued on May 15, 2026.

The 2027 NBPP includes the following provisions, amongst others:

Aligns regulation with provisions of HR1 impacting non-citizen eligibility for APTC

Reintroduces stayed and sunsetted provisions from the 2025 Marketplace Integrity and Affordability Rule, including additional income verification requirements, Failure to Reconcile (FTR) and elimination of the special enrollment period for low-income individuals

Increases federal oversight of marketplaces and insurers, including the new State Exchange Improper Payment Measurement (SEIPM) program

Requires additional actuarial reporting within rate filing justifications from insurers that silver load premiums to account for unfunded CSRs

Permits QHPs certification of multi-year Catastrophic plans and non-network plans

Disallows state-mandated EHB benefits (and requires state defrayal of these benefits) and prohibits routine adult dental coverage as an EHB

Codifies expanded eligibility for hardship exemptions that allow enrollment in Catastrophic plans for consumers age 30 or older

Permits Bronze and Catastrophic plans to exceed statutory maximum cost-sharing limits

Makes FFM-only changes, including increased special enrollment period verification, new oversight for brokers and removal of standardized plans

Updates annual risk adjustment and other technical parameters

Reduces administrative requirements for states newly transitioning to a state-based marketplace model

I covered the proposed 2027 NBPP rule in detail a couple of months ago; I’ll be addressing the final version again soon separately.

The Centers for Medicare & Medicaid Services issued a request for information (RFI) soliciting feedback on potential regulatory changes intended to reduce fraud in federally funded health care programs.

The RFI was issued on February 27, 2026, and the public comment period was open through March 30,2026. The State Marketplace Network, a collective of 21 state-based marketplaces across the country, which includes Get Covered Illinois, submitted a comment.

Marketplaces, including Get Covered Illinois, are deeply committed program integrity and currently implement a broad array of measures to prevent fraud on the front end and root out fraud on the back end to safeguard our programs. Below are some of the measures Get Covered Illinois and many other SBMs employ to keep our programs and the people we serve secure:

Strict eligibility and enrollment verification protocols

Active, ongoing oversight of brokers and assisters

Verification of applicant identity through robust identity proofing

Ongoing eligibility checks using trusted electronic data sources

Annual tax reconciliation requirements

Compliance education for staff, vendors and partners

Anonymous fraud, waste and abuse reporting

Required multifactor authentication (MFA) for all privileged users

Annual programmatic and financial oversight by independent auditors

Again, I’ll be writing more about the Trump Regime’s claims of “widespread” fraud on the ACA marketplace separately soon.

And now we get to the meat of this post:

Plan Year 2026 Enrollment Update

During the 2026 open enrollment period, Illinoisans faced unprecedented rising health coverage costs due to policies implemented by the Trump Administration and Congressional Republicans.

Despite increased costs, 448,568 Illinoisans enrolled in coverage during the annual open enrollment period. This number reflects individuals who effectuated into coverage and those with coverage pending effectuation at the end of open enrollment.

The following slides provide an update on enrollment activity from the end of open enrollment through May 31

Enrollment declined by 17%, largest decrease in nearly a decade

Federal policies, including the expiration of Enhanced Premium Tax Credits, tariffs and restrictive eligibility rules, drove up costs leading to the largest marketplace enrollment decrease since 2018.

As of May 31, 2026, 373,065 Illinoisans were enrolled in health coverage through Get Covered Illinois.

I’ll explain this further below, but it’s important to remember that the 17% refers to the drop between the number of people who select plans during Open Enrollment and those who had effectuated coverage as of May, which isn’t quite the same thing.

Customers who actively shopped retained coverage at a higher rate.

Since open enrollment ended, 83.5% of enrollees who actively shopped during open enrollment retained their coverage vesus 73% of passive auto-renewed enrollees.

The highest percentage of disenrollments (64%) were due to nonpayment of premiums.

28% of enrollees voluntarily disenrolled for reasons such as gaining job-based coverage or moving out of the state.

Disenrolled customers also include those who lost eligibility due to failure to submit required documentation (5%) and those who became newly eligible for Medicaid (3%).

Disenrollments for nonpayment in 2026 were higher than disenrollments for all reasons in prior years

Because Congressional Republicans allowed the enhanced Premium Tax Credits to expire, returning customers encountered an average 78% premium increase, making coverage unaffordable for many.

This led to an unprecedented number of customers disenrolling for nonpayment, more than all disenrollments for any reason in prior years.

Enrollees with lower incomes were more likely to end their coverage.

The largest group of disenrollments occurred among those with incomes between 100% and 150% FPL. This signals low-income enrollees struggled to absorb cost increases.

Additionally, Illinoisans with incomes over 400% were no longer eligible for financial assistance, leading to disenrollments in this category.

77% of those surveyed cited high premiums as the reason for ending their coverage.

As a state-based marketplace, Illinois invested in health coverage affordability

Illinois implemented premium alignment for plan year 2026, allowing Illinoisans to access higher Premium Tax Credits to enroll in more affordable Gold and Bronze plans. This allowed Illinois to blunt some of the impact of the federally induced premium hikes for our residents.

As a state-based marketplace, Get Covered Illinois was able to invest in targeted public outreach and enrollment assistance that helped thousands of residents move to more affordable plans with richer benefits.

While our efforts reduced the average premium increase from 78% to 26%, federal policies still left too many Illinoisans unable to afford their health coverage.

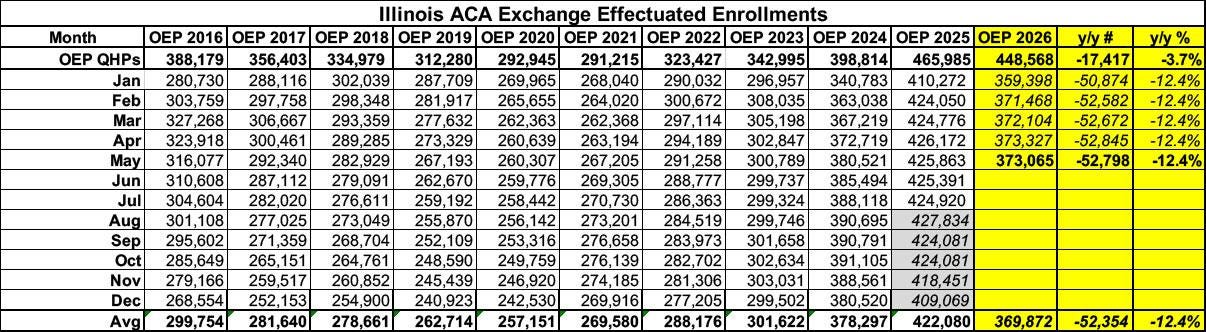

Here’s what Illinois’ enrollment looks like as of May compared compared with the official CMS monthly effectuated reports from prior years. It’s important to note that for 2026 I only have the effectuated number for May; I’m assuming January - April were proportional.

Officially, Qualified Health Plan (QHP) selections during Open Enrollment were only 3.7% lower than they were at the end of OEP 2025. However, as I expected and have warned about repeatedly, the year over year drop in effectuated enrollment as of May 2026 is over 3.3x higher...down 12.4% v.s May 2025:

What might this look like for the rest of the year? Well, here’s a visual version of the graph above, with the dotted lines respresenting what the rest of 2026 will look like if the effectuation pattern for the balance of the year follows either last year (2025) or the last pre-COVID year (2019):

If it follows 2025’s pattern, effectuations will taper off at around 358,000 by December and will average around 370,000 for the year...down 12.4% compared to 2025.

If, on the other hand, it follows the 2019 model, December effectuations will be down to just 336,000 and the average for the year will be around 359,000...down 14.8% y/y.

Here’s where things stand so far...

Arkansas: OEP down 3.8%; May effectuations down 5.3%

California: OEP down 2.6%; February effectuations down 8.5%

Colorado: OEP down 1.9%; March effectuations down 6.1%

Georgia: OEP down 12.3%; April effectuations down 28.1%

Illinois: OEP down 3.7%; May effectuations down 12.4%

Maryland: OEP up 3.4%; April effectuations down 6.3%

Massachusetts: OEP up 3.7%; April effectuations down 4.3%

Minnesota: OEP down 8.1%; February effectuations down 8.6%

Nevada: OEP down 5.8%; May effectuations down 11.1%

New Jersey: OEP down 0.8%; April effectuations down 11.6%

New Mexico: OEP up 18.1%; May effectuations up 5.6%

New York: OEP down 4.9%; May effectuations down 8.7%

Pennsylvania: OEP up 1%; May effectuations down 5.2%

Vermont: OEP down 7.7%; April effectuations down 11.5%

Washington: OEP down 5.9%; February effectuations down 15.7%

In terms of year over year average monthly effectuated enrollment as of the months of the latest data:

Arkansas: Down ~7,700

California: Down ~110,000 (down ~132,000 as of March; updated post coming soon)

Colorado: Down ~13,400 (down ~15,900 as of April; updated post coming soon)

Georgia: Down ~370,000

Illinois: Down ~52,000

Maryland: Up ~7,000 (up ~2,500 as of May; updated post coming soon)

Massachusetts: Up ~1,600 (down ~2,400 as of April; updated post coming soon)

Minnesota: Down ~10,000

Nevada: Down ~11,500

New Jersey: Down ~57,000

New York: Down ~14,500

New Mexico: Up ~7,200 (up ~6,300 as of June; updated post coming soon)

Pennsylvania: Down ~2,300 (down ~7,700 as of June; updated post coming soon)

Vermont: Down ~3,700

Washington: Down ~33,000

Adding now on the continuing Paragon fraud stuff, (from my other comment this post), the issue has been picked up now by Jonathan Cohn this morning

(here: https://www.thebulwark.com/p/obamacare-phantom-menace-aca-fraud-trump-oz-insurance-coverage ; note behind a bulwark Substack paywall)

and thus the issue of the fraud stuff coming back, perhaps now to be used to claim stopping fraud as the reason for the large enrollment drops, has gotten wider exposure.

(Jonathan's Substack has a broader audience than Gaba, as he manages a consistent approach designed for a broader audience, without those big tables of numbers in the Gaba tables that make some of the less wonky people, unfortunately, faint.)

--

(In case you don't know already, the Gaba Substack, the xpostfactoid Substack, and even my own little Substack have been mentioned in the footnotes, and possibly elsewhere as well, in the text of Jonathan's post.)

I enjoyed the post.

I'll plop down miscellaneous, not-particularly-important comments:

1) This was a nice tidbit:

"Since open enrollment ended, 83.5% of enrollees who actively shopped during open enrollment retained their coverage vesus 73% of passive auto-renewed enrollees."

2) I like your style of plot, which I think you do for all states when there is effectuated-enrollment data for the state, labelled here: "Illinois effectuated enrollment by month and year", with the two dashed lines extrapolating 2025 effectuation pattern and 2019 effectuation pattern. That's very useful.

2b) Actually, in this notorious Paragon updated report on fraud on the ACA exchanges, ( https://paragoninstitute.org/wp-content/uploads/securepdfs/2026/06/The_Persistent_Obamacare_Enrollment_Fraud_RELEASE_V1.pdf )

they seem to be doing roughly the same 2019-pattern analysis and come up with (p. 37):

"Because of the expiration of the COVID-era subsidy boosts and the buildup of substantial

improper and phantom enrollment, enrollment attrition will likely return closer to pre-COVID

patterns. Assuming an 18 percent decline from this year’s open enrollment in 2026 would

result in average monthly effectuated enrollment of about 19 million people in 2026—an

amount still 90 percent higher than the pre-COVID average."

However, you, I, numerous others view that drop to 19 million, being a drop of a few million, as a problem. But, no such point of view from Paragon. They have:

"Allowing the enhanced COVID-era ACA subsidy boosts to expire was a prudent policy change."

(the rest of the paragraph is:

"The exchanges remain heavily subsidized, particularly for lower-income enrollees, and the

underlying ACA subsidy structure continues to provide substantial premium assistance. In

HealthCare.gov states, taxpayers still cover roughly 94 percent of premiums for the median

subsidized enrollee, while nearly 70 percent of enrollees face monthly premiums below $100.

The evidence presented in this report suggests that the exchange market remains saturated

with subsidies, particularly for individuals claiming income between 100 and 150 percent FPL."

which does not make the case! )

2c) People not familiar with the fraud allegations, the latest Paragon report (link above), the apparent delay of some CMS data on coverage drops missing from a report where it has appeared in the past, and the CMS-internal leaked information that the administration was preparing to claim that the coverage drops were from the administration's successful efforts to combat fraud, I have my own post trying to put that info together:

https://normspier828307.substack.com/p/loss-of-aca-coverage-after-republicans , if interested.

2d) People who subscribe to (and know and love) Andrew "xpostfactoid" Sprung on Substack might also find the new Paragon report interesting, and it might give them a warm-and-fuzzy feeling, because Andrew is mentioned there in that report.

Extracting part of the text of that Paragon report,

"Notable ACA tracker and supporter Andrew Sprung also supports this theory"

I have been able to determine Andrew is not in full agreement with the report, based on his last posting:

https://xpostfactoid.substack.com/p/on-writing-off-newly-uninsured-americans .

As well, he indicated has further postings on the topic coming.