🚨 Washington State: Preliminary 2027 *gross* ACA rate filings are out, and it ain't pretty...

Gross is an apt word...

Hoo boy. the Washington Insurance Dept isn’t burying the lede here:

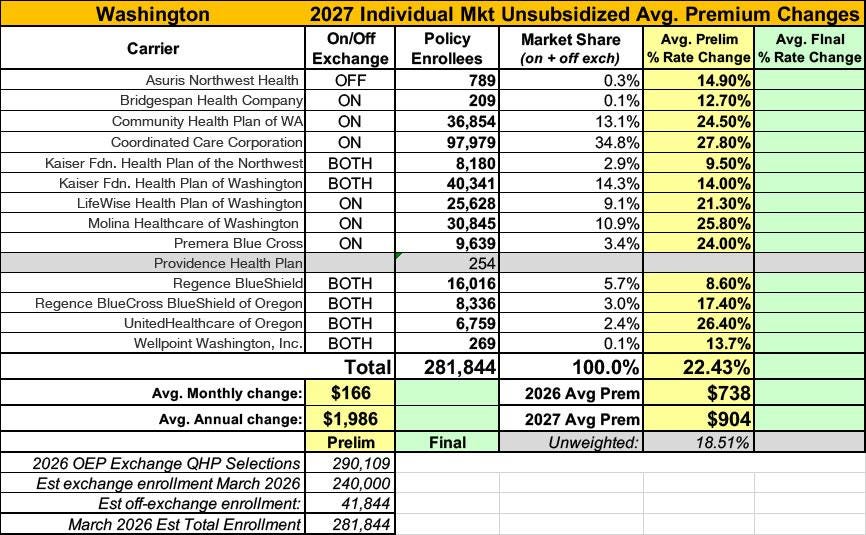

Thirteen health insurers request average 22.4% rate increase for 2027 individual market

OLYMPIA, Wash. — Thirteen health insurance companies have requested an average rate change of 22.4% for Washington state’s 2027 individual health insurance market. Insurers base requested rate changes on assumptions made about the services their policyholders will use and the cost to deliver that care.

“I know the requested rate changes will be difficult for individuals and families,” said Insurance Commissioner Patty Kuderer. “We’re going to spend the next several months reviewing every assumption made by the insurers to make sure their requests are justified.”

Fourteen insurance companies offered individual plans last year. One of those plans — Providence Health Plan, which had 254 enrollees — will not offer coverage in 2027.

More than 280,000 people in Washington do not receive health insurance through their employer and must buy coverage from the individual market. Nearly 250,000 of them shopped through the Washington Health Benefit Exchange last year. That figure was down 13% from 2025 after Congress failed to renew the Enhanced Advanced Premium Tax credits.

Ninety percent of people buying plans through the Exchange were in a Cascade Care plan in 2026, up from 79% in 2025. Cascade Care plans (standard plans) give Washingtonians a better alternative to health plans with high out-of-pocket costs and a low number of covered services. Cascade Care Savings (state premium assistance) is available through the Exchange for households at or below 250% of the Federal Poverty Level.

The Office of the Insurance Commissioner is currently reviewing the requested changes and will complete its review in September, before open enrollment in November.

ASIRUS NW HEALTH:

4.3: Proposed Rate Changes

This filing proposes an average annual rate change of 14.89% on January 1, 2027, for the Individual line of business, as shown in “Exhibit A1: Development of 2027 Rate Change.” The 2027 projected average premium is $875.38 per member per month (PMPM).

...Based on OIC guidance, only on-exchange Silver plan premium should be increased to cover the additional costs associated with providing benefits to all Silver plan enrollees, in the event the CSR subsidies are not funded. In 2027, ANH is offering plans off-exchange only, and therefore no additional load for CSR has been applied to any plan.

...Reasons for Proposed Rate Change

The following components are the most significant factors contributing to the proposed rate change: medical trend and utilization and financial experience.

Medical Trend and Utilization: These adjustments refer to what is commonly known as healthcare trend. They reflect contractual changes in the payments to healthcare providers and expected changes in the volume and types of services utilized by a carrier’s members.

Financial Experience: Each year ANH evaluates the most recent financial results in the Washington Individual market and incorporates that information into pricing.

Changes in Geographic Factors: ANH evaluates the impact of changes in the rating area factors using current enrollment and incorporates that change into pricing.

Market Morbidity: ANH expects increased market morbidity due to the discontinuance of enhanced Premium Tax Credits as well as increased provider coding activity.

Change in Benefits: Each year ANH evaluates the cost sharing features and benefits of each plan offering to determine the expected cost of incurred claims by plan.

It’s worth noting that Asuris doesn’t even offer plans on the ACA exchange anyway, so the fact that they still expect there to be “increased morbidity” for their handful of enrollees due specifically to the enhanced federal tax credits expiring is especially telling.

BRIDGESPAN HEALTH:

This filing proposes an average annual rate change of 12.65% on January 1, 2027, for the Individual line of business, as shown in “Exhibit A1: Development of 2027 Rate Change.” The 2027 projected average premium is $1113.77 per member per month (PMPM).

...This filing assumes Cost Sharing Reduction (CSR) payments will not be paid in 2027. If changes are made to the premium subsidies, risk adjustment, or reinsurance, the proposed rates in this filing may need to change materially to ensure adequacy with expected market costs.

...Based on OIC guidance, only on-exchange Silver plan premium should be increased to cover the additional costs associated with providing benefits to all Silver plan enrollees, in the event the CSR subsidies are not funded. See the “CSR Funding” section for more detail.

...Reasons for Proposed Rate Change

The following components are the most significant factors contributing to the proposed rate change: medical trend and utilization and financial experience.

Medical Trend and Utilization: These adjustments refer to what is commonly known as healthcare trend. They reflect contractual changes in the payments to healthcare providers and expected changes in the volume and types of services utilized by a carrier’s members.

Changes in Geographic Factors: ANH evaluates the impact of changes in the rating area factors using current enrollment and incorporates that change into pricing.

Financial Experience: Each year BridgeSpan evaluates the most recent financial results in the Washington Individual market and incorporates that information into pricing. The experience also includes the impacts of pooling BridgeSpan with Regence BlueShield (RBS).

Market Morbidity: BridgeSpan expects increased market morbidity due to the discontinuance of enhanced Premium Tax Credits as well as increased provider coding activity.

Changes in Benefits: Each year, BridgeSpan evaluates the cost sharing features and benefits of each plan offering to determine the expected cost of incurred claims by plan.

If the wording seems familiar, it’s because BridgeSpan is actually a subsidiary of Cambria Health Solutions...which also owns Asuris Northwest Health...as well as Regence, which means that at least four of the 13 carriers offering ACA plans in Washington next year are actually subsidiaries of the same company. Asuris and BridgeSpan combined only have around 1,000 enrollees in WA this year, however.

COMMUNITY HEALTH PLAN OF WA:

The overall proposed rate change for 2026 across all plans is 24.52%. There are approximately 36,854 members who would receive a rate change to their premiums ranging from -4.3% to 32.8% (for the same age), with rate changes varying by plan and rating area. CHPW is renewing its Complete Gold, Vital Gold, Silver, and Bronze Cascade Select Public Option plans in 2027.

...Changes in medical service costs were driven by expectations for medical inflation (cost per service and utilization of medical and pharmacy services), provider contracting, and care management. Average annual medical/pharmacy inflation of 6.3% is reflected in these rates.

...CHPW will continue to offer the Cascade Select Complete Gold, Vital Gold, Silver, and Bronze plans in plan year 2027. Benefits and member cost-sharing for these plans are set forth by the Washington Health Benefit Exchange. Changes for 2027 include the following. The cost sharing changes below may also impact premium rate changes.

...The enhanced premium subsidies first introduced through the American Rescue Plan Act (ARPA) and later extended by the Inflation Reduction Act (IRA) expired at the end of 2025, resulting in a reduction in the overall market size in 2026. We anticipate further market size reduction in 2027. We assume this will lead to increasing average statewide morbidity in 2027 relative to the 2025 experience period by 2% each year. We anticipate the remaining risk pool in 2027 to have higher healthcare needs, on average, as healthier consumers are more likely to lapse coverage. Given these considerations, we applied a morbidity adjustment to reflect anticipated changes in statewide average morbidity in 2027 relative to 2025. [note: the adjustment for this is 9.7%]

...The WA OIC introduced new Essential Health Benefits to the state benchmark plan for PY2026: Human donor milk, hearing aids and hearing exams, and artificial insemination...We modeled adjustments to projected claims to reflect the anticipated impact of these new essential health benefits. [adjustment: 0.01%]

COORDINATED CARE CORP:

Number of Individuals Impacted by Rate Increase: 97,979 individuals (membership as of March 2026)

The rating structure has not changed from 2026 to 2027; premium rates are developed based on the benefit plan, geographic area, age, and tobacco use of the insured. Premiums are charged for each individual in a family, but for no more than the three oldest dependent children under age 21. The rating factors for benefit plan and geographic area have changed. Age factors have not changed. Tobacco factors have changed to reflect that premiums no longer vary based on tobacco use. Renewing plans in 2027 will see rate changes, which vary depending on the plan selected and the member’s location in the state. The average rate increase is 27.82%.

...The estimated average annual premium per policy in calendar year 2027 is $10,562.

...Impact of eAPTC Expiration: To account for eAPTC expiration prior to the 2027 benefit year, we have assumed rates will increase due to anticipated reductions in enrollment, both at the issuer and single risk pool level. As eAPTCs expire and enrollees subsequently face increased out-of-pocket premiums, we assume healthier individuals who tend to be more price sensitive will leave the market, worsening the average morbidity of the individual risk pool.

Noticing a pattern here?

KAISER FOUNDATION HEALTHCARE PLAN OF THE NORTHWEST:

...The filed overall average premium rate change for January 1, 2027, is 9.5%. We have estimated that premium rate changes by member for those enrolled as of March 2026 will range between 7.69% and 10.90%, including the impact of benefit and cost sharing changes.

...The state of Washington has implemented a 1332 Waiver (1332) which allows formerly ineligible residents access to state funded premium subsidies when enrolled in the Cascade Gold or Cascade Silver On-Exchange plans. The projected impact on membership can be seen in the Individual Supplemental Checklist for 1332 Waiver Reporting and is consistent with the total market growth projections demonstrated in the state’s 1332 application.

This rate filing assumes that the Individual Mandate will continue to be powerless with no replacement provision for the 2027 plan year. Additionally, this rate filing assumes that the Cost Share Reduction (CSR) Subsidies will continue to be un-funded for the 2027 plan year, only people eligible for the 87% and 94% CSR plans will be allowed to enroll in On-Exchange Silver plans and additional plan paid claims costs due to CSR’s will be applied only to the On-Exchange Silver plans.

Side note: This is an important reminder that the federal individual mandate penalty technically still exists on paper...it’s just that the amount of the penalty was reduced to $0 or 0.0% of household income back in 2019, so the “penalty” itself is literally nothing.

KAISER FOUNDATION HEALTH PLAN OF WASHINGTON:

...All silver plans offered in the Exchange and only silver plans offered in the Exchange are loaded for cost-share reduction subsidies.

As of March 2026, there were 40,341 enrollees that will be impacted by the 2027 rate change. The average requested rate increase estimated for members enrolled as of March 2026 is 14.03%. The rate increase varies by plan from -19.65% to 18.56%.

...With the proposed rate change, Kaiser Foundation Health Plan of Washington projects an overall loss ratioo percentage of 87.64% and an ACA medical loss ratio (MLR) of 89.6% in 2027. The overall loss ratio is not the same as the 2027 federal MLR. It is calculated as incurred claims / (risk adjustment + premium) and represents the average loss ratio across all products using 2027 projected enrollment for each plan.

Side note: This is an important reminder that while the ACA requires insurance carriers to spend at least 80% of their premium revenue on actual medical claims (and to refund the difference if they come in below that threshold on a 3-year revolving basis), many carriers are spending significantly more than 80% on claims.

...The enhanced premium tax credits that were extended by the Inflation Reduction Act expired at the end of 2025. However, we have included no additional load in the morbidity assumptions in Worksheet 1. For plan year 2026 and 2027, there is a mandated 43.6 percent silver load for on-exchange plans, significantly increasing the premium for the benchmark plan and thereby making bronze and gold plans more affordable for members receiving premium subsidies. Between the increased subsidies and the already low uninsured rate in Washington, our best estimate is that neither the population nor its average morbidity will materially change in plan year 2027.

Note that Kaiser of WA is the first carrier I’ve seen which specifically says they don’t anticipate any further rate hikes to be caused specifically by the tax credit expiration.

LIFEWISE HEALTH PLAN:

LifeWise is in 31 counties and has 25,628 individual members on metallic plans as of March 2026. In 2027, LifeWise will exit King County for all plans.

The average rate increase for 2027 is 21.2%. This is driven by higher medical and pharmacy costs, increased utilization, demographic shifts, benefit design changes, and changes in anticipated risk adjustment transfer dollars.

...Cost-sharing components (including deductibles, copays, coinsurance, and out-of-pocket maximums) for renewing plans have been adjusted to meet the metallic actuarial value (AV) and mental health parity requirements. These types of changes are needed as cost and utilization of health care change every year.

In 2027, the deductible for the LifeWise Essential Gold plan is increasing by $200. For the LifeWise Essential Bronze plan, the deductible is increasing by $200 and the out-of-pocket maximum is increasing by $400.

For the Cascade and Cascade Select plans, deductibles are increasing by the following amounts:

Complete Gold ($700), Vital Gold ($300), Silver ($300), and Bronze ($100). The out-of-pocket maximums are increasing by: Vital Gold ($2,900), Silver ($1,450), and Bronze ($1,650). For the Bronze plan, the mental health office visit copay is increasing by $5.

...In last year’s rate filing, a Morbidity Adjustment of 1.089 was applied. This was to cover the impact of the expiration of the enhanced advanced premium tax credits in 2026, which LifeWise expected to cause healthy people to exit the market or purchase less expensive plans. We now know what plans members purchased in 2026, and we do not expect further deterioration in 2027.

OK, that’s another carrier saying the same; sounds like it varies widely depending on how bad the specific carrier anticipated the risk pool damage to be this year.

MOLINA HEALTHCARE OF WASHINGTON:

Molina is requesting on average a 25.84% premium increase for its individual policies sold in the Washington Marketplace effective January 1, 2027. 30,845 Molina Marketplace members would receive changes to their premiums ranging from a 24.24 percent increase to a 26.62 percent increase depending on their geographic location and metal tier. Molina will renew the Molina Cascade Complete Gold, Molina Cascade Silver, and Molina Cascade Bronze plans, and Molina Cascade Vital Gold for 2027. Finally, please note these are averages, by plan and due to members aging, premium changes could be larger or smaller than anticipated.

...Changes in Medical Service Costs: Medical and pharmacy combined trend of 13.8 percent was applied in the development of the rates for expected increases in the utilization and cost of covered services. 4.5 percent of the total trend is due to utilization. 8.8 percent of the total trend is due to unit cost, largely driven by a 19.8% trend in pharmacy drug cost.

...The Molina Cascade Complete Gold plan is being renewed with changes such as deductible from $1000 to $1,700.

The Molina Cascade Silver plan is being renewed with changes to the out-of-pocket maximum on Silver 100, from $2,400 to $4,000, Silver 150, from $2,850 to $4,000, Silver 200, from $7,950 to $9,600, Silver 250 from $9,750 to $11,200.

The Molina Cascade Bronze plan is being renewed with changes to the out-of-pocket maximum from $10,150 to $11,800.

The Molina Cascade Vital Gold plan is being renewed with changes to the out-of-pocket maximum from $8,800 to $11,000

...The morbidity of Molina’s covered population is expected to increase between the experience period and the projection period. Enhanced Premium Tax Credits (ePTCs) expired at the end of 2025. Molina retained Milliman to analyze the impact of expiring premium subsidies on statewide morbidity from 2025 to 2026. We reviewed the study and applied a 1.023 adjustment to the experience to base period acuity adjustment.

PREMERA BLUE CROSS:

Premera is in 10 counties and has 9,639 members on metallic plans as of March 2026. In 2027, Premera will expand to an additional 15 counties, adding coverage in Adams, Asotin, Benton, Columbia, Ferry, Garfield, Grant, Kittitas, Lewis, Pend Orielle, San Juan, Snohomish, Stevens, Walla Walla, and Whitman Counties.

The average rate increase for 2027 is 24.0%. This is driven by higher medical and pharmacy costs, increased utilization, demographic shifts, benefit design changes, and changes in anticipated risk adjustment transfer dollars.

...No Morbidity Adjustment is applied in the 2027 rate development. In last year’s rate filing, a Morbidity Adjustment of 1.050 was applied. This was to cover the impact of the expiration of the enhanced advanced premium tax credits in 2026, which Premera expected to cause healthy people to exit the market or purchase less expensive plans. We now know what plans members purchased in 2026, and we do not expect further deterioration in 2027.

A demographic shift adjustment of 1.159 is made for the expected change in membership demographic between the experience and projection period. This includes the impact of expanding into multiple counties, and development details are in Appendix 2.2.

PROVIDENCE HEALTH PLAN:

As I wrote about last week, Providence Health Plan is shutting down their entire health insurance division across the Northwest. While most of their business is in Oregon, they do have a few hundred ACA enrollees in Washington State as well who will have to shop for new coverage this fall.

REGENCE BLUESHIELD:

Regence BlueShield (Regence) is filing a rate change request for its Individual metallic products. These plans comply with federal Affordable Care Act (ACA) plan design and benefit requirements, and Regence has approximately 16,000 members enrolled in this line of business as of March 2026. Regence is projecting total enrollment for 2027 to be approximately 192,200 member months. This filing is based on claims experience from January 2025 through December 2025, with claims paid through March 2026.

The projected average rate change for plans effective in 2027 is 8.64%, which is an average rate change of about $72 per member per month (pmpm). Because 8.64% (or about $72) is an average, it is possible to have a different rate change. Rate changes vary from about 1.8% to 13.5% and this variability in rate changes is driven by plan design and geographic factor changes. Factors affecting a member’s premium are age, family composition, plan, and geographic area. Expected cost differences by product are updated every year to ensure premium differences are appropriate.

...Market Morbidity: RBS expects increased market morbidity due to the discontinuance of enhanced Premium Tax Credits as well as increased provider coding activity.

REGENCE BLUECROSS BLUESHIELD OF OREGON:

The projected average rate change for plans effective in 2027 is 17.37%, which is an average rate change of about $144 per member per month (pmpm). Because 17.37% (or about $144) is an average, it is possible to have a different rate change. Rate changes vary from about 10.9% to 20.9% and this variability in rate changes is driven by plan design and geographic factor changes. Factors affecting a member’s premium are age, family composition, plan, and geographic area. Expected cost differences by product are updated every year to ensure premium differences are appropriate.

...Market Morbidity: RBCBSO expects increased market morbidity due to the discontinuance of enhanced Premium Tax Credits.

UNITEDHEALTHCARE OF OREGON:

UHCOR is filing 2027 rates for individual products. The proposed rate change is 26.41% and will affect 6,759 individuals. The rate changes vary between 24.39% and 28.09%. Given that the rate changes are based on the same single risk pool, the rate changes vary by plan due to plan design changes.

...Morbidity Adjustment: The Morbidity Adjustment factor is 1.195 as shown on Worksheet 1 of the URRT.

An adjustment was applied to account for anticipated changes in UHCOR internal morbidity levels. The adjustment was developed by comparing risk scores normalized for demographics and benefits. The factors used in the calculation of the adjustment are consistent with that of the risk adjustment transfer calculation described in Section 4.3.6.

...EXPIRATION OF ENHANCED SUBSIDIES AND OTHER REGULATORY CHANGES

An adjustment was applied to account for the expiration of enhanced premium subsidies passed under the American Rescue Plan Act (ARP) and extended by the Inflation Reduction Act (IRA). Due to the expiration of the enhanced premium subsidies effective 1/1/2026, UHCOR observed a decline in enrollment due to higher post-subsidy premiums. Healthier members are expected to leave at a disproportionately higher rate than those with significant healthcare needs, increasing market morbidity in 2026. This estimate is based on internal modeling using historical Wakely National Risk Adjustment Reporting (WNRAR) data, Marketplace Open Enrollment Period Public Use Files, and Wakely early enrollment reporting for 2026. The adjustment factor is 1.101.

WELLPOINT WASHINGTON:

This submission applies to Wellpoint’s individual market rates available for sale January 1, 2027. The composite rate change proposed in this filing is 13.7%, as shown in Worksheet 2, Section I of the URRT (row 22). Table 2.1 summarizes the significant factors driving the proposed composite rate change effective January 1, 2027.

... An average morbidity adjustment that calibrates the manual experience to expected average morbidity in the Washington individual market. We used CMS risk adjustment reports to derive this adjustment (accounting for the mix underlying Elevance’s 11 manual rate states).

• We anticipate a reduction in the overall market size in 2027 due to the 2026 expiration of the enhanced premium subsidies first introduced through the American Rescue Plan Act (ARPA) and later extended by the Inflation Reduction Act (IRA). This will lead to increasing average statewide morbidity in 2027 relative to the 2025 manual rate experience as consumers will either lose access to subsidies (for those at or above 400% of the Federal Poverty Level) or face higher net premiums due to less generous subsidies. We anticipate the remaining risk pool in 2027 to have higher healthcare needs, on average, as healthier consumers are more likely to lapse coverage. Given these considerations, we apply a morbidity adjustment of 1.031 to reflect anticipated changes in statewide average morbidity in 2027 relative to the manual rate experience.

• An adjustment that reflects the expected morbidity of members that will purchase Wellpoint’s plans (relative to the statewide average morbidity in the Washington individual ACA market). This is derived from historical data Elevance has regarding the morbidity of new members they enroll once entering a new market. This analysis was also used to develop the risk adjustment payment that is projected for 2027.

Add all of this up and Washington’s ~280,000 individual market enrollees are looking at seeing gross premiums jump by another 22.4% next year, assuming the preliminary filings are approved as is.

IT’S IMPORTANT TO REITERATE THAT THIS IS FOR UNSUBSIDIZED ENROLLEES ONLY. This year around 64% of ACA exchange enrollees in Washington receive federal subsidies, which amounts to around 55% of the state’s total individual market when you include the ~40K or so off-exchange enrollees.

Washington tends to publish annual rate filings for their small group market sometime after their individual market filings are made public, so that’ll have to wait.

This is literally insane. I am curious what this will look like for California.

I happened to take a look at the list of filings

https://fortress.wa.gov/oic/consumertoolkitrt/Search.aspx

and noticed it includes both small employer plans, and individual (ACA on exchange) plans.

And, from a perusal, it looks like the small employer plans also have very steep increases. (I see 16% on one, 20% on another. I have only looked at a few.)

A natural question to ask, (even though it has been answered fallaciously by the notorious graph referenced here: https://normspier828307.substack.com/p/senate-republican-leader-john-thune )

is, are the ACA plans rising faster than small employer AFTER taking into account the increased adverse selection from the expired expanded subsidies AND lower enrollment causing higher administrative costs?

(I have not looked at all the filings myself, and I suspect they do not all list the proportion of the increased due to this lapse causing increased adverse selection or lower enrollment causing higher administrative costs, but I see some do have at least the former.)

--

The importance of the comparison is that there are allegations that the ACA structure causes excessive cost growth. If small employer also has the same trend (after taking into account the increased adverse selection on ACA plans), then we might see that the problem extends at least to small employer as well (as regulated in Washington state). It may even be suggestive of costs growing out-of-control at the current moment all through the healthcare system.

(If costs are growing out-of-control at the current moment all through the healthcare system, that is also worth knowing.)